Based on reported import licenses, US flat products imports rose 47% from 468,000 short tons in April 2020 to 687,000 tonnes last month. The highest volume increase came from hot roll where volumes rose mainly from Canada, but also from Japan. Hot dip galvanized imports also rose significantly due to higher volumes from Canada and Mexico.

Flat products imports in the first four months of 2021 were 12% higher than in the same period last year. Imports of cut plate rose 49%, imports of hot rolled increased 27%, and imports of hot dip galvanized rose 1%. In contrast, cold rolled imports fell 10%.

Steel Imports Monitor US Flat Products Import Licenses

The hot topic of the day in the steel industry is steelmaking raw materials, and this week’s featured dataset focuses on DRI, one of the key steelmaking materials for the future production of sustainable steel.

The dataset “Midrex World Direct Reduction Statistics” has all the statistics publicly available from Midrex‘s World Direct Reduction Statistics report. This includes production by product (CDRI, HBI, HDRI), by shaft furnace producer (MIDREX, Other), and by process (MIDREX, HYL/Energiron, PERED, Other, Rotary Kiln), together with DRI shipments by product (CDRI, HBI) and transport means (Water, Land).

In addition, the dataset includes DRI production by country since 1990. In the chart below, you can see the steep increase in Indian and Iranian DRI production over the last 10 years.

Worldsteel reported crude steel production in China at 94 million metric tonnes in March, 19% higher than in March 2020. Chinese crude steel output in the first quarter of 2021 was 12% higher than in the same period last year.

Data from China’s General Administration of Customs show net finished steel exports in March at 6.2 million tonnes, 17% higher than in March 2020. Net finished steel exports in the first quarter of 2021 were 26% higher than in the first quarter of 2020.

China Monthly Crude Steel Production, 2006 to 2021

China produced 94 million tonnes in March, accounting for 56% of world output and rising 19% on March 2020. In other parts of Asia, Indian output rose 24%, while Japanese and South Korean production both increased 5%.

European Union (27) crude steel output rose 17.5% on last March following a 10% rise in Germany and a 69% increase in Italy (Italian source Federacciai). North American production rose 0.1% with US output up 1%. Other significant changes compared to March, 2020 include a 9% increase in Turkey and Russia, as well as an 11% production rise in Iran.

Upper bell Blast furnace Völklingen Ironworks, 2012, by Borvan53, CC0, via Wikimedia Commons

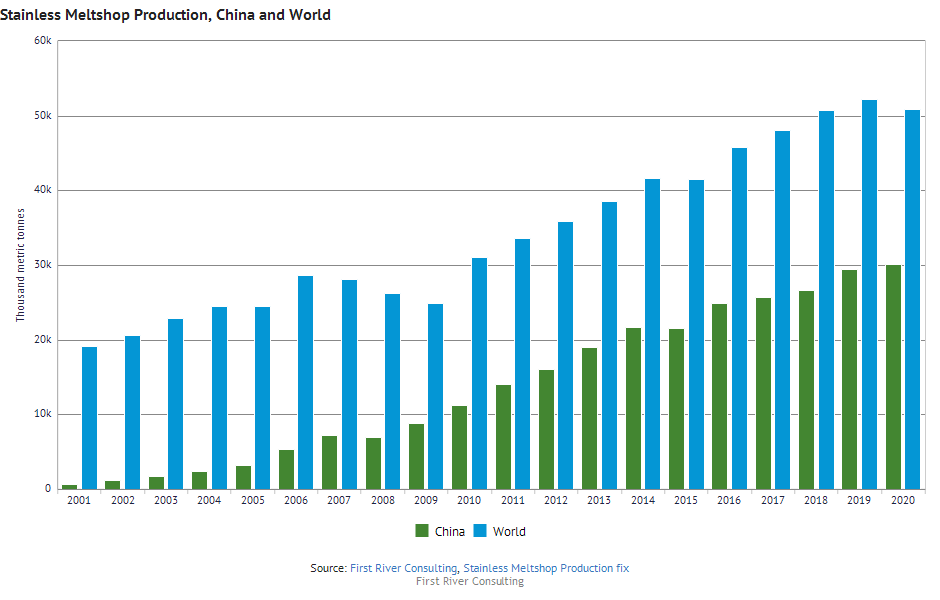

Did you know that stainless steel meltshop production worldwide in 2020 was 50.9 million metric tonnes, a 2.5% drop from 2019 levels? Did you know that world stainless meltshop production grew annually by 5% on average between 2001 and 2020? You can find all this data in this week’s featured dataset, Stainless Meltshop Production.

Stainless Meltshop Production figures come from the International Steel Stainless Forum (ISSF) and include stainless meltshop production (slab/ingot equivalent) quarterly and annually from 2001 worldwide and in specific regions and countries. You can easily create exceptional charts like the one below, which illustrates how China’s share of world stainless production has risen from 4% in 2001 to 59% in 2020.

If you’d like to see what other great steel industry data is available in the Steel Data Room, try a free Steel Data Room trial.

Based on reported import licenses, US long products imports rose 29% from 219,000 short tons in March 2020 to 282,000 tons last month. Licenses indicate that the increase was mainly due to higher rebar imports which rose significantly from Algeria, Portugal, and Turkey.

US long products imports in the the first 3 months of 2021 were 6% higher than in the same period last year with the largest increases coming from rebar and all other structural sections imports.

US long products import licenses from ITA Steel Import Monitor

January 2015 to March 2021

Short tons

A crate of bent and somewhat rusty rebar at construction site in Rixö old quarry, Lysekil, Sweden by W.carter, CC BY-SA 4.0 https://creativecommons.org/licenses/by-sa/4.0, via Wikimedia Commons